T2 preparation guide for Canadian small corporations

A T2 return is not just a form. For an owner-led corporation, it is a preparation workflow: gather records, map financial activity, resolve questions, review the output, and keep support for later.

OPTAX organizes that workflow around five objects.

1. Records

Start with the materials that explain the corporation's year:

- bank and credit card activity;

- bookkeeping exports;

- receipts and invoices;

- financial statements;

- asset purchase records;

- shareholder loan details;

- prior-year context when available.

The goal is not to upload everything forever. The goal is to bring in enough records for reviewable preparation.

2. Evidence

Evidence is what connects a number or classification back to a source.

Useful evidence looks like:

- a transaction linked to a statement row;

- a receipt attached to an expense;

- a GIFI mapping with visible source context;

- an owner confirmation for a classification question;

- a note explaining why an item was left for CPA review.

If the package cannot explain where an important number came from, it is not ready.

3. Questions

Questions are not a failure state. They are how the workflow avoids pretending uncertain items are settled.

Common examples include:

- personal vs. business use;

- missing receipts;

- shareholder loan details;

- asset purchases that may require CCA review;

- unusual transactions that need professional judgment.

Good preparation makes those questions visible before package generation.

4. Review

Review is where the owner checks the package and decides whether a CPA should be involved.

For simple corporations, owner review may focus on completeness and source support. For complex situations, review should include a CPA or qualified professional before decisions are made.

OPTAX should make that handoff easier by keeping records, evidence, questions, and notes together.

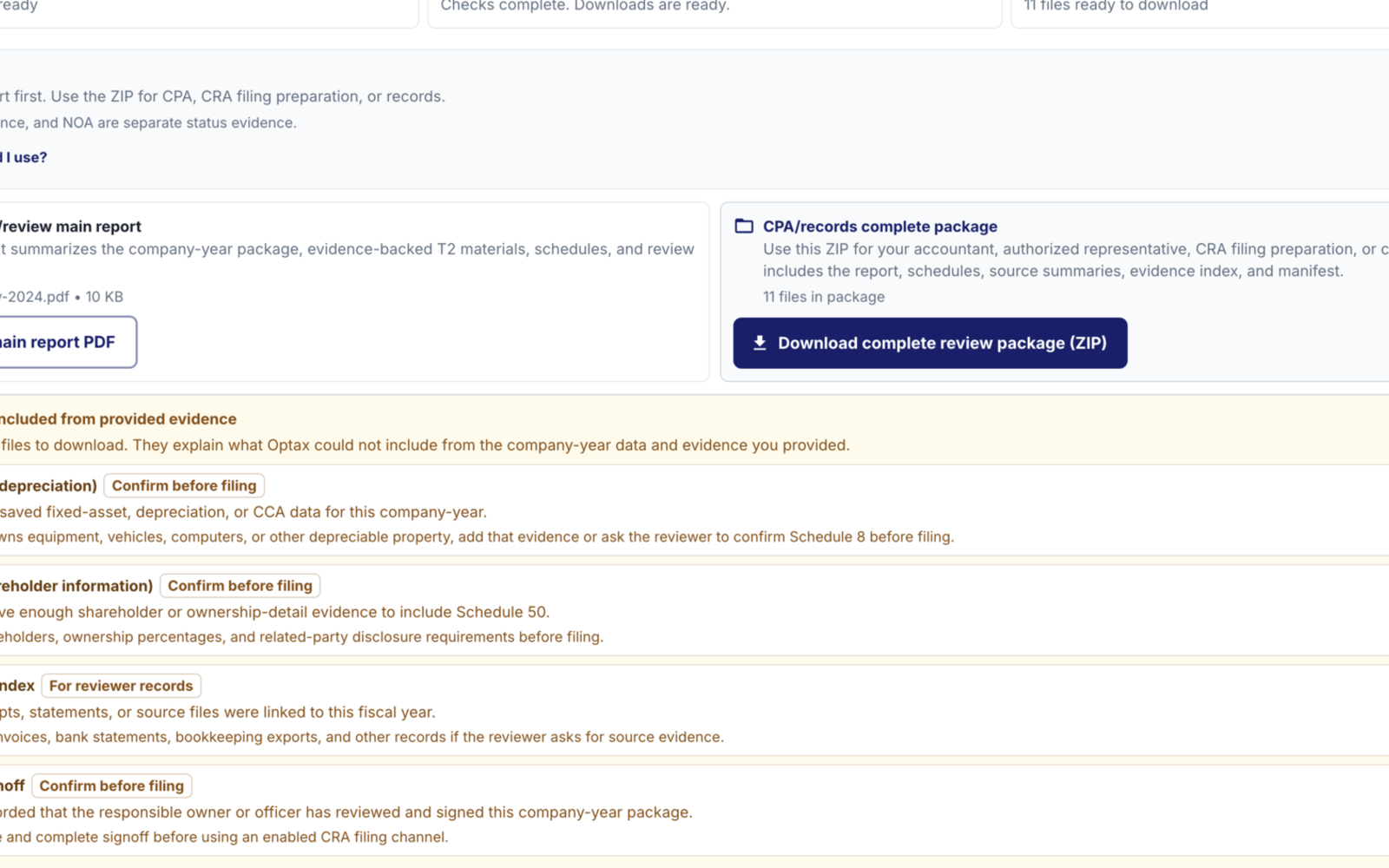

5. Package

The package is the output: T2 preparation materials, GIFI mapping, review notes, and supporting records.

That package is not a CRA filing confirmation. It is a review-ready set of materials for the owner or authorized representative to inspect before submission through CRA channels.

Useful CRA references

CRA guidance says a corporation generally has to file its T2 return within six months after the end of its tax year. Any balance owing may be due earlier, commonly two or three months after year-end depending on the corporation's situation.

Always confirm deadlines against the CRA and your corporation's facts before relying on a date.

Official starting points:

- CRA: Corporation income tax return

- CRA: When to file your corporation income tax return

- CRA: Balance-due day

How OPTAX helps

OPTAX is designed to make the preparation path visible:

Records -> Evidence -> Questions -> Review -> Package.

That is the work a small corporation needs before a T2 package feels ready to review.

Boundary

This guide is general information, not tax advice. OPTAX prepares and organizes materials for review. Complex matters should be reviewed by a qualified tax professional.